This post is for all the fact-loving, data-crunching guys who keep claiming that tech is a merit-based ecosystem where anyone with a good idea who is willing to bust their tail 80 hours a week will succeed.

Are you smart? Are you impressed with those considered brilliant?

Do you look for signs of genius in your kids?

Can you really tell at an early age?

Monday was Albert Einstein’s 137th birthday.

Einstein was nicknamed “der Depperte” — the dopey one — by the family maid, because he was slow to learn to talk.

He couldn’t find a job teaching, so worked in the patent office in Bern, Germany, while he wrote some of his most important papers.

He was still there when he wrote the paper that underlies E=mc2.

He didn’t get an offer to teach for another four years — and almost didn’t accept because of the low salary and his description to a friend isn’t exactly complimentary.

“So, now I too am an official member of the guild of whores.”

Although Einstein’s family knew he was famous that didn’t understand why. His answer when his son asked him offers great insight to his attitude.

“When a blind beetle crawls over the surface of a curved branch, it doesn’t notice that the track it has covered is indeed curved. I was lucky enough to notice what the beetle didn’t notice.”

Entitlement was neither part of his life nor of his beliefs. He was a socialist and detested and fought the discrimination so rampant in his adopted US homeland.

He lived by his values, expeditious of not, and died by them, too, when he refused treatment (an attitude the “live forever tech crowd” should embrace).

“It is tasteless to prolong life artificially. I have done my share, it is time to go. I will do it elegantly.”

That was back at the end of February and in tech three weeks can be a lifetime.

The new news is that Talmon Marco founder of Viber six years ago and sold for $900 million two years later, is the guy behind Juno, Uber’s newest competitor — but a competitor that values it’s people.

“What Uber left out in the process of building their company is that they completely and totally forgot about the people who do the work, the drivers. Imagine a company where all the employees hate management; that is not a good place to be.”

And there lies the problem for most of the 1099 crowd.

Unlike most other 1099 businesses, full-time Juno drivers will be employees, not contractors, receive stock quarterly and have the potential to build “as much equity as the founders.” according to Marco.

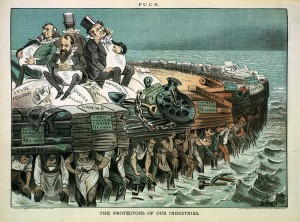

Remember the robber barons of the late 19th-arly 20th Century?

A robber baron is a wealthy, powerful businessman who employs practices including exerting control over natural resources, influencing high levels of government, paying subsistence wages, squashing competition by acquiring competitors, creating monopolies and raising prices [emphasis mine], and schemes to sell stock at inflated prices to unsuspecting investors.

Even the inflated stock seems familiar when you consider that Uber’s unicorn valuation is based on funds raised, not revenue, and it’s losing hundreds of millions each year.

It’s amazing to me, but looking back over the last decade of writing I find posts that still impress, with information that is as useful now as when it was written. Golden Oldies is a collection of what I consider some of the best posts during that time.

Eight years have passed since I wrote this, but it still holds true. Gen Y is eight years older and its leading edge are already producing Gen Z, which will continue the disruption, make unimaginable demands on the workplace and eventually become the status quo. That’s just the nature of the beast. Read other Golden Oldies here

I love it. Another article focusing on what companies need to do to hire Gen X and Y—of course they’re a big chunk of the workforce and getting bigger—Gen Y alone is 80 million strong and will compose 44% of workers by 2020.

Not that I disagree with the comments, but that the focus is strictly on doing these things in order to lure younger employees because they demand it, when the same perks[listed at this link–Ed] will attract works of any age.

‘The move often is aimed at attracting the youngest members of the work force — Generations X and Y — who are more outspoken than their baby boomer predecessors about demanding a life outside the office, said Lynne Lancaster, co-author of When Generations Collide.’

What people seem to forget is that the Boomers were plenty disrupting and more demanding than their parents—in fact, historically each generation has disrupted the status quo and demanded more than its predecessor in one way or another.

Just as every generation has focused on various traits of the upcoming generation and deemed them the end of civilization—if not the world.

I’m sure our hunter ancestors looked with horror at their gatherer children and predicted starvation if the herds weren’t followed.

I have no problem when Gen X and Y talk their demands and walk when they aren’t met because most of those demands will improve the workplace for all ages, but they would do well to remember that eventually they will become their parents—maybe not to themselves, but to the newer generations agitating for change.

I’ve been around startups since the late 1970s; long before dot com and software took over the spotlight.

And what I learned about VCs back then was different from VCs now.

Back them, most VCs were guys who had started or helped start companies, with strong operational, not just technical, and strategic background.

Sad to say, most VCs with under 25 years experience often don’t know what they’re doing, because they have never created/built a company, while the rest are just bankers masquerading as VCs following “sure bets.”

Granted, VCs have always had much in common with lemmings, preferring to fund “me, too,” companies, as opposed to earth-shattering, high risk products/services that actually moved society in new directions.

From my perch back then on the edge of the VC ecosystem I watched as the “names on the door” retired and were replaced by Wall Street wunderkinds, whose only skill was manipulating money.

What didn’t change was their lemming-like, follow-the-leader investment strategy.

Things haven’t improved much.

While more partners and “names on the door” have operational experience, the investment ecosystem is more closed-door incestuous than ever before.

So unless you are one of the mostly white, mostly male, right school, strongly connected, entitled few, start your company with a bootstrap mentality from the beginning — not as a fallback contingency.

Waiting for funding is like asking for permission.

First, a disclaimer: this post is in no way a recommendation for the University of Phoenix. In fact, I have long been against for profit education, especially UP, which is not only the largest, but one of the worst.

That said, I’d like to strip the logos from the new ad running on national TV and make it required watching for every boss in every business, whether large or small.

It’s amazing to me, but looking back over a decade of writing I find posts that still impress, with information that is as useful now as when it was written. Golden Oldies is a collection of what I consider some of the best posts during that time.

The idea of managers as coaches responsible for encouraging and facilitating their people’s professional development has grown into a major movement. One question remains the same. Read other Golden Oldies here

How much management/coaching is too much?

I hear that question a lot.

Most managers want to do a good job and are looking for ways to improve.

But, as one commented recently, if you do everything recommended by the experts you would use so much of each person’s time that productivity would tumble and even the best coaching would have a negative impact.

Which is why I say that management and coffee are similar.

The right amount of management/coaching is good for the brain in that it provides challenges that foster growth; it also lowers frustration and stress, which enhances mental and physical health.

According to the research, the “right” amount of coffee is around 20 ounces a day, i.e., one venti-size Starbucks.

That equates to the most effective management/coaching, which provides all the information needed to do the job at one time (not more nor less) and then gets out of the way while staying accessible if needed.

Many of the coffee-fueled are more likely to drink three to five ventis a day, which is detrimental to health and longevity.

A comparable amount of management/coaching is detrimental to health, productivity and retention.

But if you’re still not sure how much coaching is best for of your people, you might resort to an old fashioned approach and discuss it with each one directly — face-to-face.

For years, venture capitalists have been pushing hypergrowth over profits, at least though the initial phases of investment rounds. Investors told Lehmann to reinvest the company’s money in pushing more growth over building a sustainable business.

That advice didn’t go far with the Postmates CEO. (…) Lehmann argues that it’s the CEO’s fundamental job to have looked at the margins and made decisions early on.

“Companies that run for the last two years in hyper growth are now wondering how to make money.”

I completely agree — hypergrowth without a hope of unit economics that lead to profitability has always been a fool’s errand with precious few exceptions, and even those had their “come to Jesus” realization points that the investors were getting nervous and were anxious for at least a hope of a repeatable, profitable set of unit economics.

There has been a sense that pushing the bidding of sequential funding rounds at ever-increasing valuations would create a kind of de-facto “momentum” and crowd-out 2nd and 3rd and 4th place contenders, or at least amass a large enough war chest to drive pricing down as much as needed to push competitors out of the running (usually also by creating such a huge and dominant brand that customer acquisition in a noisy market is too expensive to make progress to catch up with the so-called leader).

This is ultimately as silly as the Texas and Miami and Las Vegas housing bubbles, that depended on “the next fool” to buy-in at a higher valuation, depending themselves on having a subsequent investor bail them out at a higher valuation, and so goes the escalator. The problem is, the escalator gets to the top at some point and there has to be a “destination” where value exists and with it, a hope of profitability.

The unsteady IPO market of last year and the continued bearishness of the IPO exit market this year has effectively called-out that “top of the escalator” and there are no more “next fools” (i.e. large enterprise buyers at the >$1 Bil level and no robust IPO appetite from capital market leaders that demand value and cash flow and a hope of profits).

So now, once again we are back to reality.

The great news about being back to reality is two-fold.

1) Sub-billion dollar valuations are no longer an “embarrassment” to VCs; and

2) Entrepreneurs can reasonably weigh a variety of capital structures that include bank and trade debt as well as investment equity and debt structures, all supported by revenue and that means free cash-flow.

With this in mind, the VCs and the investment community in general must start to become “reasonable,” because they are suddenly back in the traditional capital markets and will have to compete with other capital sources and structures for the hot deals.

Middle and nascent deals will have to become cash-flow generating, and for this reason they will also (wisely) become more reluctant to give up huge chunks of equity just to bring in working capital (at least not until the enterprise value pops to a higher tier by using bank debt, trade debt and other creative capital structures).

Savvy entrepreneurs and founding teams will also be less excited about creating an early and dramatic bump in valuation just to bank growth capital, because a down-round will likely wipe out a giant proportion of their equity. The giddy “we are a unicorn” has turned into “what happens in a down round?” reality check, that most people forgot about. Early venture investors have protected their downside with special preferred terms that founders and exec teams rarely consider or can demand. If this were real-estate, it might even start to look like over-aggressive venture investors that pump up valuations too early, only to have the market adjust to “reasonable” later, were “predatory.” It is an interesting parallel that will not be lost on founding teams, angel investors and early exec team members that hope to be rewarded via their equity stake.

The reticence to of many of the younger venture investors (those with fewer than 20 years of experience) having yet to bring in a 5X or 10X much less a Unicorn, to invest in early stage deals, is now balanced by the abundance of crowdfunding and syndicate fundraising at the seed and angel level. This is a great organic re-shaping of the investment and capital markets in favor of the early stage company and entrepreneur.

There is also a growing recognition that the early stage deals that do get picked up by venture investors have been in a long slow decline and “narrowing” of deals to known insiders and repeat successful (i.e. “brought a good exit to a venture fund’) founders. I think that this is largely common sense (bet on the horse that won the last race for you), and also based on the reality that it is a rare and elite breed of entrepreneur that can see an opportunity and execute a successful solution. That said, a close examination of the venture deals that have been funded in favor of known founders pales next to the stats behind the successful new ventures that have been founded by first time startup teams. The difference is largely that part of the value-add from the venture investors is the addition of those “experienced” startup executives onto the exec team as soon as the big money comes into play. Thus the risk of execution is somewhat reduced.

What does that mean to today’s startups? It means that the old concepts of cash-flow, repeatable and scalable selling and service delivery models, the idea of managing customer acquisition, retention and lifetime customer value, are again in vogue.

As they should have always been. While there will continue to be many good reasons for companies to temporarily sacrifice cash flow and profitability for raw user or customer growth, the days of “just get 1 million users and we’ll figure out how to make money later” are – at least for the time being, gone. And we celebrate that.

Unit economics always wins. This goes back to the days of “the lemonade stand” cash-flow exercise. It’s what built the world’s greatest capital markets. And it will always remain the best place to start. Water, sugar, lemons, cups and napkins. And a sign and a cardboard box. “How many cups of lemonade must we sell at what price to pay for the supplies, time and sign?” Simple. One does not need an MBA or to be a dropout PhD candidate to start with those basic principles.

In another parallel with the real estate (mortgage) market, today’s startup teams should be asking themselves the same questions that prudent investors will be asking them (kind of like the new mortgage market, where everyone has to go through “full documentation” to get a standard mortgage loan):

How can I make money? How can I do it at scale? What is my selling process and is it repeatable? Who will pay for my service or product and what will they pay, and why? How much money do I need in working capital to find my perfect product-market fit and establish the right selling model and price point/margin? What are the unit economics of my business? What drives retention and churn? What prevents others from copying me and disintermediating my base? Is there a brand value that creates loyalty, or is this market driven by other values and factors? What are my logical exits? Who are the logical acquirers? Is there a realistic IPO path?

Yes, we are back to reality. It sucks for some people. And that’s okay. Those people should get with the program or get out of the startup business. Disrupt and question everything. Be bold, revolutionary, even bombastic and disrespectful of the incumbents and status quo. But don’t ignore the fundamental rules of business that underly the path all companies must tread to go from small to large, and startup to profit and successful exit. After all is said and done, you have to make payroll. Sell to a customer a second time. Own a brand people love and trust.

Reality only sucks because it makes you work harder to win, and forces you to confront inconvenient tasks and difficult questions. Short cuts are nice but when they don’t work you end up falling off of a cliff. Better to work harder than run headlong at a cliff you can’t see coming.

Entrepreneurs face difficulties that are hard for most people to imagine, let alone understand. You can find anonymous help and connections that do understand at 7 cups of tea.

Crises never end.

$10 really does make a difference and you’ll never miss it,

What people seem to forget is that the Boomers were plenty disrupting and more demanding than their parents—in fact, historically each generation has disrupted the status quo and demanded more than its predecessor in one way or another.

What people seem to forget is that the Boomers were plenty disrupting and more demanding than their parents—in fact, historically each generation has disrupted the status quo and demanded more than its predecessor in one way or another. We all need things that inspire us when we are so tired or depressed that we don’t want to get out of bed, let alone put on a happy face.

We all need things that inspire us when we are so tired or depressed that we don’t want to get out of bed, let alone put on a happy face.

{kind=link}